Exits, 2/27/2026

How we did on the trades we exited this week, and some lessons learned.

This Week’s Trade Exits

As soon as I exit a trade, I note that in the comments of the post where I first mentioned the trade; at the end of the week, I try to track them all in one post. Starting in July, 2024, I have also been tracking them in this spreadsheet. These are the trades I exited this week.

Stocks or Exchange Traded Products

None.

Options

Put spread on Eos Energy Enterprises (EOSE 0.00%↑). Entered at a net credit of $2.10 as part of a 3-leg combo on 11/10/2025; assigned and exercised on 2/27/2026. Loss: 100% of max risk (91% of premium collected). Signal: Multibaggers.

Put spread on Rocket Lab USA (RKLB 0.00%↑). Entered at a net credit of $2.50 as part of a 4-leg combo on 2/4/2026; assigned and exercised on 2/27/2026. Loss: 100% of max risk (100% of premium collected). Signal: PA Top Names.

Put spread on Baidu (BIDU 0.00%↑). Entered at a net credit of $1.65 as part of a 4-leg combo on 2/2/2026; assigned and exercised on 2/27/2026. Loss: 100% of max risk (203% of premium collected). Signal: PA Top Names.

Short calls on uniQure (QURE 0.00%↑). Sold-to-open for $3.97 as part of a 4-leg hybrid combo on 12/16/2025; bought-to-close for $3.50 on 2/26/2026. Profit: 12%. Signal: Multibaggers.

Short calls on uniQure (QURE 0.00%↑). Sold-to-open for $6.47 as part of a 4-leg hybrid combo on 11/25/2025; bought-to-close for $2.34 on 2/26/2026. Profit: 64%. Signal: Multibaggers.

Short calls on Personalis (PSNL 0.00%↑). Sold-to-open for $0.65 as part of a 4-leg hybrid combo on 2/11/2026; bought-to-close for $0.15 on 2/23/2026. Profit: 77%. Signal: Multibaggers.

Short calls on KVH Industries (KVHI 0.00%↑). Sold-to-open for $1.10 as part of a 2-leg calendar call spread on 12/12/2025; bought-to-close for $0.20 on 2/24/2026. Profit: 82%. Signal: Multibaggers.

Put spread on Opera (OPRA 0.00%↑). Entered at a net credit of $1.10 as part of a 3-leg combo on 12/1/2025; exited at a net debit of $0.15 on 2/27/2026. Profit: 86% (return on max risk: 68%). Signal: Chartmill.

Put spread on Abivax (ABVX 0.00%↑). Entered at a net credit of $4.25 as part of a 3-leg combo on 1/28/2026; exited at a net debit of $0.05 on 2/27/2026. Profit: 99% (return on max risk: 73%). Signal: Multibaggers.

Calls on Viavi Solutions (VIAV 0.00%↑). Bought for $1.80 as part of a 3-leg combo on 1/9/2026; sold (half) for $11.20 on 2/27/2026. Profit: 522%. Signal: PA Top Names.

3-leg combo on SandRidge Energy (SD 0.00%↑). Entered at a net debit of $0.05 on 12/18/2025; exited the April put spread at a net debit of $0.20 on 2/19/2026 and the July calls for $3.40 on 2/23/2026. Profit: 7100% (return on max risk: 139%). Signal: Chartmill.

Comments

Stocks or Exchange Traded Products

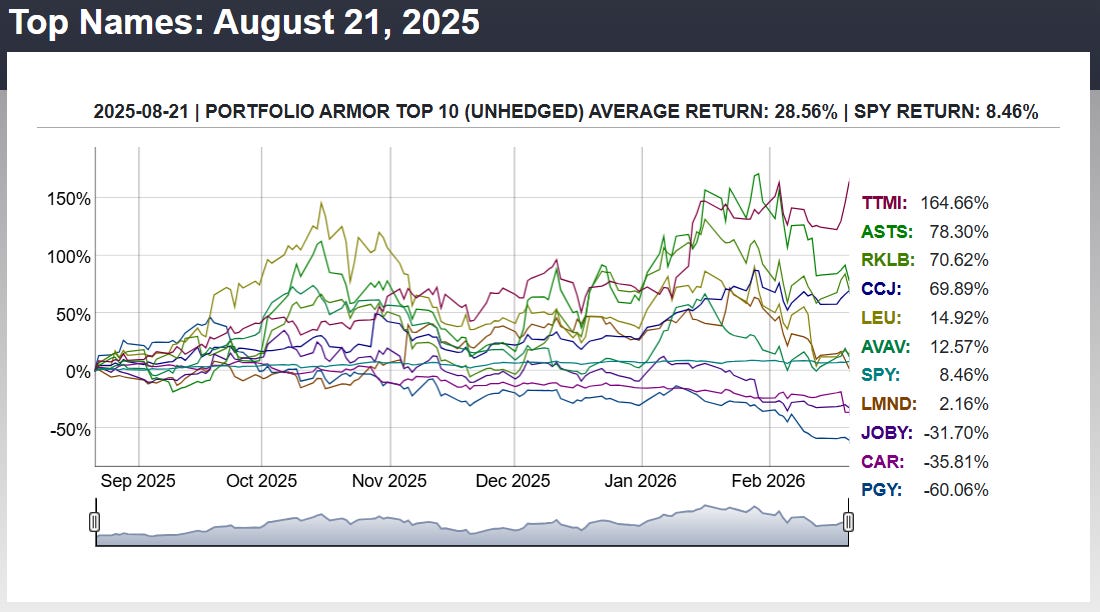

No exits this week, as I haven’t been doing our basic strategy, which involves buying stocks and ETFs, and have been focusing on options instead. Nevertheless, the performance of our system’s top names have nearly doubled that of the SPDR S&P 500 Trust (SPY 1.32%↑) since I started this Substack. Here’s the performance of our last weekly Top Names cohort to finish its 6-month run:

You can find the performance of all 139 weekly Top Names cohorts that have finished their 6-month runs here.

Options

Options Structures For A Whipsaw Market

This was a good week to be reminded why we’ve leaned so hard into financed call structures—3-leg combos, and 4-leg hybrids with calendars—rather than just naked calls. On the one hand, we took three full losses on near-dated put spreads (EOSE, RKLB, BIDU). That’s the cost of renting downside floors in front of binary or macro headlines: sometimes the floor pays for the ceiling, and sometimes the floor just burns down. On the other hand, the same basic template—long, farther-dated calls financed by nearer-dated short premium—gave us a string of chunky wins on the income side: the short calls in Personalis, KVH Industries, and both uniQure structures, and very high-percentage gains on the Opera and Abivax put spreads. In a whipsaw environment where momentum names gap violently in both directions, these hybrids have done what they’re supposed to do: let us harvest high front-month volatility, take partial profits into spikes, and when the underlying drops, remove upside caps cheaply while keeping the long calls working.

Cashing In On Convexity

Two trades stand out as examples of that: the Viavi calls and the SandRidge 3-leg combo. In both cases, defined-risk entries gave us the confidence to sit through noise while the thesis played out, and the structure let us turn modest initial debits into asymmetrical outcomes—including a 500%+ gain on the first half of our Viavi calls. Those are the kinds of payoffs that justify a few 100% losses on put spreads: we’re deliberately trading a book where the losers are capped and the winners can be open-ended.

The Cost Of Questioning Our Own Rules

The one place we second-guessed our own rules this week was uniQure. Raising the buy-to-close targets on the short calls based on anticipated FDA headlines was a speculative override of our usual “let it bleed toward $0.20” discipline. In hindsight, that decision left money on the table: the stock got hit on a TV soundbite that may not even have been about the right program, and we ended up paying more than we needed to to close the calls. The lesson there isn’t to avoid names with binary catalysts—those are often where the best asymmetry lives—but to be very sparing about loosening our exits on short premium just because the story feels exciting. Going forward, the default remains the default: keep buy-to-close levels tight, treat overrides as rare exceptions, and let the structures do the work.