Trading Through Epic Fury

How we’re navigating volatility during the Iran war.

Trading Through The Iran War

Volatility has surged. Our core themes haven’t broken.

When we wrote about the war with Iran last weekend, investors were still trying to figure out whether this would be a brief shock or the start of a broader and more durable risk event.

Nearly a week later, we still don’t have complete clarity, but we do know a few things.

First, this war is real enough to matter for markets. U.S. stocks have been pressured as investors weigh higher energy prices, renewed inflation fears, and the possibility of a prolonged conflict. Oil has also moved sharply higher as traders price in supply disruption and shipping risk tied to the Gulf and the Strait of Hormuz. Reuters has reported this week on surging oil and gas prices, shipping disruption, and broader market stress tied to the conflict. (Reuters)

The Market Is Adjusting To A Real War

Second, the market is starting to adapt. That doesn’t mean the risk is gone. It means that once a geopolitical shock stops being hypothetical and becomes part of the daily tape, investors begin repricing specific exposures instead of just hitting the whole screen.

We’ve already seen that dynamic in recent market action: stocks have remained volatile and are still on track for steep weekly losses, but the tape has also shown bursts of stabilization as traders react to shifting expectations around the duration of the war, diplomacy, and energy-market intervention.

That matters, because from our perspective the big picture hasn’t actually changed very much.

Our Core Themes Still Look Intact

Our core themes remain intact: reindustrialization, AI buildout, embodied AI, defense tech, and biotech. The war has added volatility to the market and, in many cases, much more volatility to individual names. But it hasn’t invalidated the underlying drivers behind those themes.

If anything, in some cases it has highlighted them. We saw that this week in the market’s reaction to few names we have positions in, such as nLIGHT (LASR 0.00%↑), a maker of high-power lasers and directed-energy systems, and BWX Technologies (BW 0.00%↑) , a supplier of nuclear components and services for defense and energy markets, where the tape reminded investors that the world still needs real hardware, real capacity, and real industrial and defense capabilities.

Why We’re Still Holding Our VIX Hedge

A week before this war started, we wrote about hedging against it, using a specific call spread on the S&P 500 volatility index, the VIX:

We’re also still holding that VIX hedge. But the longer this war continues, the less likely I think a truly catastrophic outcome becomes.

That may sound counterintuitive, but here’s what I mean. Iran has relatively little incentive to “hold something back” now that it is openly at war with both the U.S. and Israel. At the same time, its capabilities are unlikely to improve as the conflict drags on. The biggest market shock tends to come from uncertainty about what might happen. Once the war is underway and the other side is already using what it has, the range of plausible negative surprises can begin to narrow—even if the headline risk remains high.

That doesn’t mean we’re complacent. It means we’re distinguishing between a market that is volatile and a market that is still likely to suffer some entirely new, much larger shock. So far, I’m leaning against the prospect of a much larger shock.

Harvesting Volatility Has Continued To Work

And that brings us to the part most relevant to traders: our options structures designed to harvest high implied volatility have continued to work during this war.

So far this week, we’ve had 10 full or partial trade exits, and 7 of them have been profitable. A few examples:

Put spread on nLIGHT. (LASR 0.00%↑) Entered at a net credit of $2.15 as part of a 4-leg combo on 2/4/2026; exited at a net debit of $0.20 on 3/4/2026. Profit: 91% (return on max risk: 64%).

Calls on Nokia Corp. (NOK 0.00%↑). Bought for $0.80 as part of a 3-leg combo on 1/21/2026; sold half for $2.50 on 3/2/2026. Profit: 213%. Signal: PA Top Names.

3-leg combo on AXT (AXTI 0.00%↑). Entered for a net debit of $2.45 on 12/29/2025; exited the February $15/$10 put spread at a net debit of $0.20 on 2/9/2026; sold the August $20 call for $28.50 on 3/2/2026. Profit: 1,055% on premium outlay (return on max risk: 338%). Signal: Market Watchers.

3-leg combo on Viavi Solutions (VIAV 0.00%↑). Entered for a net debit of $1.15 on 1/9/2026; exited the February $17/$15 put spread at a net debit of $0.16 on 1/28/2026; sold half of the June $19 calls for $11.20 on 2/27/2026 and the second half for $16.00 on 3/2/2026. Profit: 1,069% on premium outlay (return on max risk: 372%). Signal: PA Top Names.

The point isn’t that every trade wins in a war. It’s that in an environment where implied volatility is elevated and single-stock reactions are violent, structures that finance longer-dated upside by harvesting rich near-term premium can still do exactly what they were designed to do. That has been a major part of how we’ve navigated this tape.

What I’m Watching In Oil

That framework also informs how I’m thinking about oil here.

If oil keeps ripping in the short term, at some point I may look to take the other side of that move and bet on a reversion toward more recent averages over the next several months, by which time I expect this war to be over. Right now, though, the options market doesn’t make that bearish bet especially attractive. The setup may improve if elevated fear keeps inflating premiums. So that’s something I’m watching—not something I’m forcing.

Reuters’ reporting this week has underscored both sides of that setup: energy prices have surged and physical disruptions have spread across shipping and refining, but policymakers are also openly discussing ways to counter extreme price spikes, and some officials are framing the energy shock as temporary rather than structural.

We’ll Keep Looking Where Our Edge Has Been

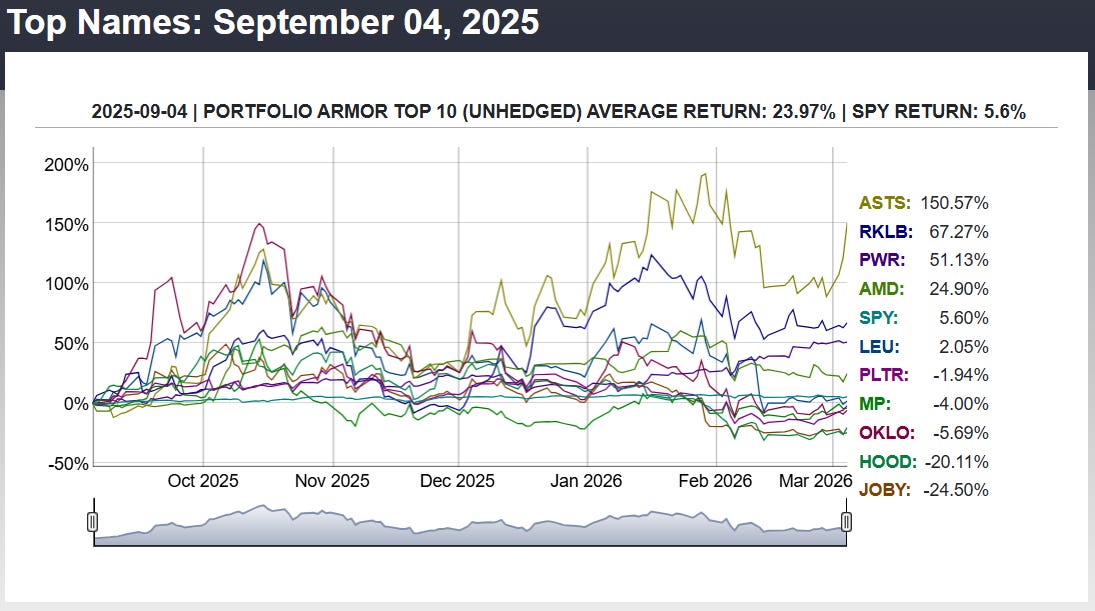

In the meantime, we’ll keep doing what we’ve been doing: looking for names from our proven sources of alpha, from Portfolio Armor’s Top Names, which have continued to outperform,

To names surfaced by our Market Watchers X list, and then structuring trades in a way that lets us harvest volatility instead of just paying up for it.

Wars create noise, fear, and violent repricing. They can also create opportunity—especially for traders who stay disciplined about themes, structure, and exits.

So far, that discipline is still working.