Top Names, 7/16/2026

A brief market comment, followed by a Top Names performance update, and this week's Top Ten Names.

War And Rotation

Last week, we wrote that the market had spent three weeks pricing the U.S.–Iran ceasefire as a peace. This week made the distinction painfully clear. The United States resumed large-scale strikes on Iran, Iran threatened additional regional energy exports, and oil rose for a fourth straight session. That geopolitical shock hit a market already rotating hard away from its former AI leaders.

Another DeepSeek Moment

The latest AI scare came from Zhipu AI, known internationally as Z.ai and its new open-source GLM-5.2 model. It offers a one-million-token context window and an architecture that cuts per-token computing requirements. That immediately revived the DeepSeek argument: if better software lets us run AI with a fraction of the hardware, perhaps the hardware buildout is being overbuilt.

If that turns out to be true—and if Jevons paradox does not apply—it would be bearish for the AI hardware stack. We should say that plainly. But GLM-5.2 does not demonstrate it. A 753-billion-parameter model with a one-million-token context window is not evidence that computing power no longer matters. It is evidence that powerful AI is getting cheaper to use. Lower costs can mean more tokens, more agents, more workloads, and more applications that were previously uneconomic. DeepSeek’s original breakthrough did not stop the current capital-spending cycle, and there is little evidence yet that this one will either.

Leverage Travels

Part of the violence has also come from Korea, where repeated semiconductor-led selloffs have contributed to seven KOSPI circuit breakers already this year, most recently on Monday, after an extraordinary run. Highly levered markets do not unwind neatly. Forced selling travels across borders and across tickers, and margin calls do not stop to ask whether next quarter’s HBM demand remains strong.

The Tape Is Damaged. Demand Isn’t.

On Wednesday, we laid out the fundamental case in “The AI Buildout Is Accelerating.”

The evidence has only gotten stronger. Micron Technology (MU) reported another enormous sequential increase in revenue and guided higher again. Penguin Solutions (PENG) reported record revenue and raised guidance. ASML (ASML) raised its full-year forecast and expanded capacity plans. And Taiwan Semiconductor Manufacturing (TSM) reported another record quarter and committed another $100 billion to U.S. chip capacity.

None of that guarantees these stocks will start going up again soon. Crowded trades can correct brutally while their underlying businesses keep improving. But the reports are evidence of demand, not its collapse. The tape is damaged. The AI buildout is not.

The Cyclical P/E Trap

The bears are right about one thing: a low trailing P/E does not automatically make a memory stock cheap. In a cyclical business, the multiple often looks lowest near peak earnings because the denominator is temporarily inflated.

But that observation only helps if earnings actually are near their peak. The real question is not whether memory is cyclical—it is—but where we are in this cycle, and whether AI demand, HBM content, capacity constraints, and longer customer commitments have extended it. Recent results and guidance make a peak-earnings assumption look premature. This may be an unusually long cycle, not the end of cyclicality.

Waiting for the P/E to rise is not a strategy, either. It can rise because the stock appreciates, but it can also rise because earnings estimates collapse. If the current cycle has further to run, waiting for a more conventionally reassuring multiple could mean missing most of the remaining move. Meanwhile, adjacent AI names with higher multiples—or no current earnings at all—have been hit much harder, which looks more like a valuation and positioning unwind than evidence that the buildout has stopped.

Better Models, More Demand

Here is one anecdotal data point from running this Substack. The biggest pain point has been tying brokerage fills back to their original trade alerts and documenting every OpEx-week exit in our posts and detailed spreadsheet. That used to take me more than a dozen hours. The latest models from Anthropic and OpenAI can now largely automate it.

Within a few hours of trying Anthropic’s latest model, I upgraded from its $20 monthly plan to its $100 plan. That is the other side of the efficiency argument: as AI gets smarter, it becomes much more useful, and users become willing to pay more for it. Efficiency does not merely save tokens. It creates customers and use cases.

Respecting The Damaged Tape

Finance X is full of victory laps from people who were not along for the climb. The vehemence of some of those victory laps says something about positioning and prior nonparticipation, but nothing about end demand. Bullish commentary can be colored by ownership too. Price action deserves respect, but it is not, by itself, proof that the underlying thesis has failed.

So we are not fighting the tape. Our recent chip and memory options trades were structured to wait out a correction for several months, if necessary. Tonight’s top ten is again heavy on AI hardware—a vote of confidence in the medium-term buildout, not a command to catch every falling knife. We’re respecting the damaged tape. Our basic strategy below has its trailing stops, and in our discretionary trades, we can wait for the setups to repair.

The AI buildout can remain intact while AI stocks correct. Both can be true.

Our Basic Strategy

Our basic strategy is to buy equal dollar amounts of the Portfolio Armor web app’s top ten names, put trailing stops of 20% or more on them, and replace them with names from the current week’s top ten when we get stopped out of a position—there are no options involved in this strategy.

Another Use For Our Top Names

We also use our top names in options trades, such as this one we exited this week:

4-leg hybrid combo on Targa Resources (TRGP 0.00%↑). Entered at a net debit of $2.45 on 4/20/2026; exited the July 17, 2026 $210/$200 put spread at a net debit of $0.20 on 5/14/2026; then sold the September $270 / July $280 call calendar for a net credit of $18.25 on 7/15/2026. Profit: 637% on net debit (125% on max risk). Signal: PA Top Names.

A Top Names Performance Update

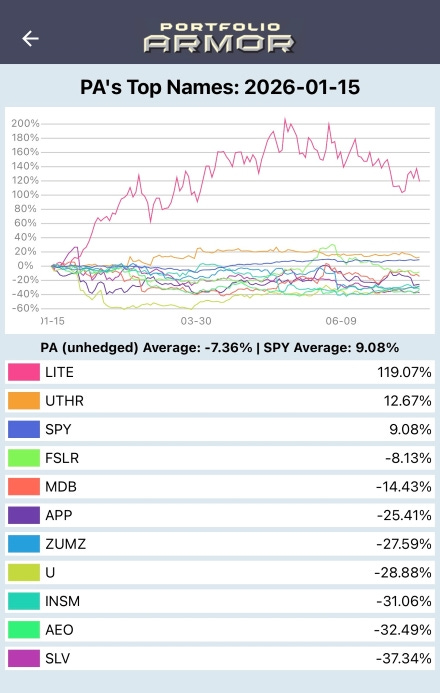

Before we get to this week’s top ten names, let’s look at the final, 6-month performance of our top ten names from January 15th.

Over the next 6 months, our top ten names from January 15th, 2026 returned -7.36%, versus +9.08% for the SPDR S&P 500 Trust ETF (SPY 0.23%↑).

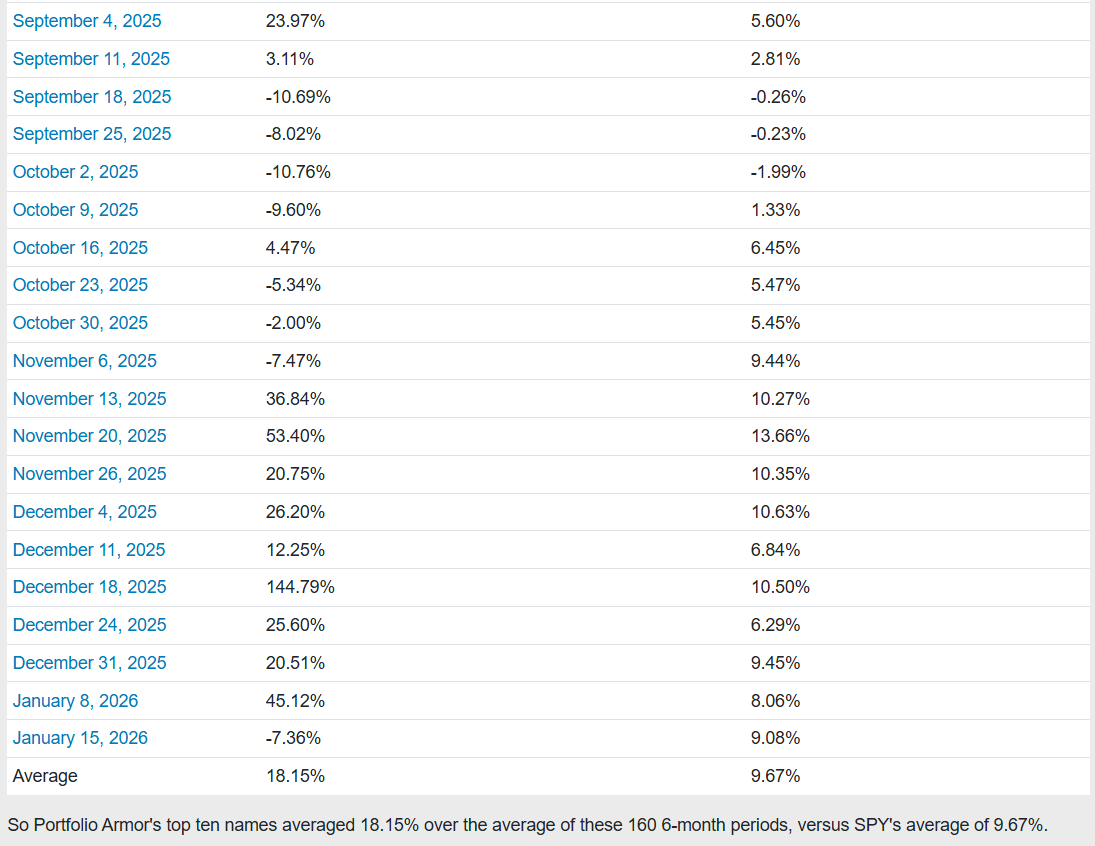

So far, we have 6-month returns for 160 weekly top names cohorts since we started this Substack at the end of December, 2022.

[Skipping ahead so this post doesn’t exceed email length—you can see the top names returns for every week here]

And as you can see above, our top names have averaged returns of 18.15% over the next six months, versus SPY’s average of 9.67%. You can see an interactive version of the table above here, where you can click on each date and see a chart showing each of the holdings that week.

This Week’s Top Names

Below are Portfolio Armor’s current top ten names as of Thursday’s close.