More Evidence The AI Boom Has Legs

AI infrastructure company Penguin Solutions' blockbuster quarter, and new memory pricing data.

Apocalypse Not Now

In “AI Apocalypse” last week, we wrote about drivers behind the sharp selloff in AI-infrastructure names.

Memory, photonics, optical networking, semiconductor equipment, power, and AI-infrastructure stocks were all hit. The bearish case was familiar: the AI buildout had run too far, expectations were stretched, and investors were starting to question how much of the capex cycle was real.

In that post, we wrote that the evidence still showed the AI buildout was real:

The evidence still says the AI buildout is real. Memory, storage, optics, power, cooling, and data-center infrastructure remain bottlenecks. The better-positioned companies are generating rapidly ramping revenue and earnings from that demand.

This week, Penguin Solutions (PENG 0.00%↑) offered more evidence of that.

Penguin Solutions’ Blowout Quarter

Most investors probably haven’t heard of Penguin. That’s part of why we like it.

Penguin Solutions is an AI-infrastructure company focused on memory, high-performance computing, and AI-factory deployment. Its platform combines infrastructure software, advanced memory, compute systems, services, and partner solutions to help customers deploy and scale AI workloads.

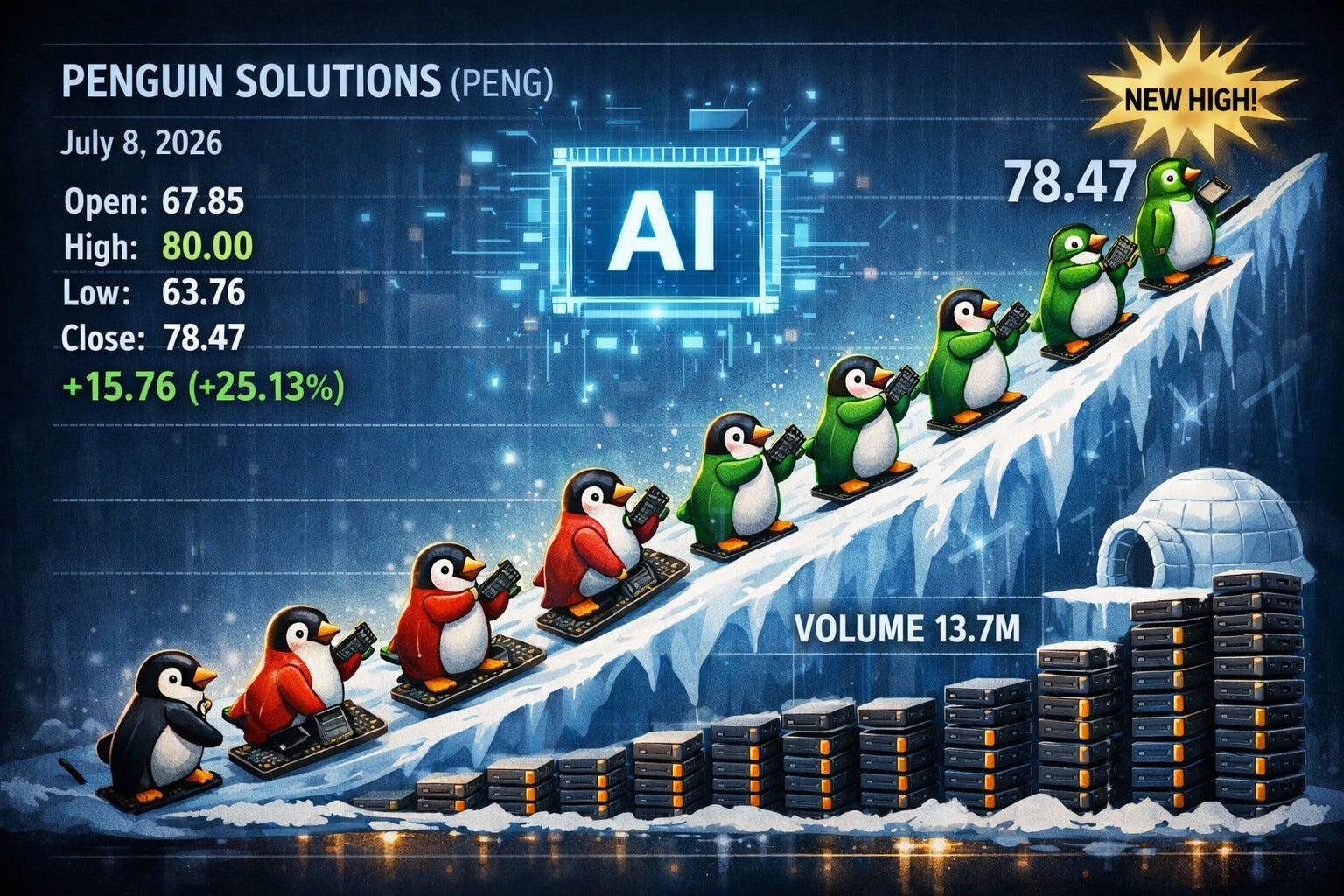

On Tuesday, Penguin reported record quarterly revenue of $479 million, up 48% from the year-ago quarter. GAAP operating income rose 417%. Non-GAAP EPS rose 79%. Management raised full-year guidance for both sales and EPS.

The stock jumped more than 25% the next day.

That market reaction is worth noting because Penguin sells into the physical layer of the AI buildout: memory, compute systems, infrastructure software, and deployment services.

CEO Kash Shaikh said Penguin’s AI Factory Platform strategy is working, that Integrated Memory sales more than doubled year over year, and that its AI Infrastructure business continued to build momentum. He also said the company is seeing “very strong AI-driven customer demand for memory and AI infrastructure solutions.”

That’s evidence.

The bearish AI narrative says demand is cracking. Penguin’s quarter says demand is still moving through the infrastructure stack.

Memory Continues To Be A Bottleneck

The most important line in Penguin’s release may have been this one:

“As inference and agentic AI workloads become more persistent and context-rich, memory is increasingly becoming one of the primary performance and scalability bottlenecks.”

That lines up with what we’ve been seeing across the AI stack.

Training got most of the early attention. Inference is where the infrastructure problem keeps expanding. More agents, longer context windows, persistent workloads, enterprise deployments, and real-time AI systems all increase pressure on memory and systems architecture.

Penguin’s numbers reflect that.

Integrated Memory sales more than doubled year over year. Penguin added four new AI Infrastructure customer logos in the quarter. It also became an NVIDIA AI Factory Specialized Partner.

Memory Pricing Data Provides More Evidence

TrendForce reported Wednesday that, according to Taiwanese media citing ADATA Chairman Simon Chen, memory makers have notified customers of another Q3 contract-price increase: DRAM up 20%–30% and NAND Flash up 35%–40%.

ADATA is a Taiwanese memory and storage company. It sells DRAM modules, SSDs, flash products, and related storage gear, so its chairman’s comments are a useful read-through on real memory-market tightness.

TrendForce’s own Q3 forecast was less aggressive than the ADATA numbers, but still pointed the same way: DRAM contract prices up another 13%–18% and NAND Flash contract prices up 10%–15%. TrendForce tied the tightness to AI server demand, AI inference, large-scale data-center deployments, and capacity being reallocated toward server applications.

That’s the backdrop Penguin is selling into.

The AI buildout isn’t just Nvidia. It’s the physical stack: memory, compute systems, networking, power, cooling, infrastructure software, and deployment services.

Penguin sits right in that layer.

How We Traded It

We included a PENG trade for Portfolio Armor subscribers in this alert on June 25th,

This was the trade:

Today’s Market Watchers Trade

AI compute infrastructure / HPC / memory systems theme

The stock is Penguin Solutions (PENG 16.51%↑), and our trade is a hybrid combo consisting of these four legs:

Buying the October 16th, 2026 $80 call,

Selling the September 18th, 2026 $85 call,

Selling the October 16th, 2026 $50 put,

Buying the October 16th, 2026 $45 put,

At a max net debit of $1.60. The max gain on 1 contract is about $1,250 (if the short September $85 call expires in-the-money; if it expires out-of-the-money, or we buy-to-close it before then, our upside will be uncapped), and the max loss is $660.

This trade filled at $1.40.

The key to understanding that structure is that the long October $80 call alone cost $13.95 then (it traded at close to $20 yesterday). Instead of simply buying that call, we sold other options around it and brought the cost of the whole bullish structure down to $1.40.

That gave us bullish exposure to the same AI-infrastructure theme while costing a tenth of what we would have paid to simply buy the call outright.

This is why we keep talking about harvesting volatility.

When these names are volatile, options get expensive. Buying that volatility outright can work, but it can also mean paying too much for the right idea. We’d rather sell part of that volatility, lower the cost of entry, and keep the upside asymmetric.

The Barbell Still Works

We’ve been describing our current approach as a barbell.

On one end, we have speculative convexity trades: smaller names where one catalyst can produce outsized returns. On the other end, we have higher-probability theme-continuation trades: companies where the theme, technicals, and fundamentals already line up.

Our recent Micron trade was an example of the second side of that barbell.

In Time To Get Back Into Micron, we wrote that the better AI-infrastructure names were still selling real products into real demand, with revenues and earnings moving sharply higher alongside their share prices.

Micron had just strengthened that point with a blowout quarter and commentary about tight memory supply lasting beyond calendar 2027.

Penguin strengthened it again this week.

The company reported record results, raised guidance, and tied the raise directly to AI-driven demand in memory and AI infrastructure. The stock’s reaction confirmed that investors understood the read-through.

Penguin was a less obvious way to express the same broader theme: AI compute infrastructure, memory systems, and the buildout of real AI factories.

The evidence keeps pointing the same way.

The AI buildout is still real. The physical stack is still seeing demand. Some of the best opportunities may be in the companies supplying the infrastructure behind the boom—not just the headline names everyone already owns.