Exits, 6/5/2026

How we did on the trades we exited this week.

This Week’s Trade Exits

As soon as I exit a trade, I note that in the comments of the post where I first mentioned the trade; at the end of the week, I try to track them all in one post. Starting in July, 2024, I have also been tracking them in this spreadsheet. These are the trades I exited this week.

Stocks or Exchange Traded Products

None.

Options

Put spread on NexGen Energy (NXE 0.00%↑). Entered at a net credit of $0.49 as part of a 4-leg hybrid combo on 3/26/2026; exited at a net debit of $0.12 on 6/2/2026. Profit: 76% (return on max risk: 25%). Signal: PA Top Names.

Put spread on Cameco (CCJ 0.00%↑). Entered at a net credit of $1.48 as part of a 4-leg hybrid combo on 3/25/2026; exited at a net debit of $0.20 on 6/2/2026. Profit: 86% (return on max risk: 36%). Signal: PA Top Names.

Short call on Capricor Therapeutics (CAPR 0.00%↑). Sold-to-open the June 18th, 2026 $40 call for $1.57 as part of a 4-leg hybrid combo that filled on 3/30/2026; bought-to-close that call for $0.20 on 6/1/2026. Profit: 87% on premium collected. Signal: Multibaggers.

Put spread on Twist Bioscience (TWST 0.00%↑). Entered at a net credit of $2.45 as part of a 4-leg hybrid combo on 2/27/2026; exited at a net debit of $0.20 on 6/4/2026. Profit: 92% (return on max risk: 88%). Signal: Multibaggers.

Short call on Perma-Pipe International Holdings (PPIH 0.00%↑). Sold-to-open the June 18th, 2026 $40 call for $3.20 as part of a 4-leg hybrid combo on 2/18/2026; bought-to-close that call for $0.20 on 6/1/2026. Profit: 94% on premium collected. Signal: Market Watchers.

Short call on Cameco (CCJ 0.00%↑). Sold-to-open at $5.00 as part of a 4-leg hybrid combo on 3/25/2026; bought-to-close at $0.20 on 6/5/2026. Profit: 96%. Signal: PA Top Names.

4-leg hybrid combo on iShares MSCI South Korea ETF (EWY 0.00%↑). Entered at a net debit of $4.84 on 3/25/2026; exited the July 17th, 2026 $115/$110 put spread at a net debit of $0.20 on 5/8/2026 and exited the October 16th, 2026 $150 / July 17th, 2026 $155 call calendar at a net credit of $13.60 on 6/5/2026. Profit: 177% (return on max risk: 87%).

4-leg combo on Sphere Entertainment (SPHR 0.00%↑). Entered at a net debit of $1.50 on 2/5/2026; exited the February 20th, 2026 $85/$80 put spread at a net debit of $0.20 on 2/12/2026 and exited the August 21st, 2026 $105/$115 call spread at a net credit of $8.00 on 6/1/2026. Profit: 420% (return on max risk: 97%). Signal: PA Top Names.

4-leg combo on Western Digital (WDC 0.00%↑). Entered at a net debit of $0.97 on 3/27/2026; exited the May 1st, 2026 $245/$240 put spread at a net debit of $0.20 on 4/14/2026 and exited the September 18th, 2026 $340/$350 call spread at a net credit of $8.00 on 6/3/2026. Profit: 704% (return on max risk: 114%). Signal: PA Top Names.

Comments

Stocks or Exchange Traded Products

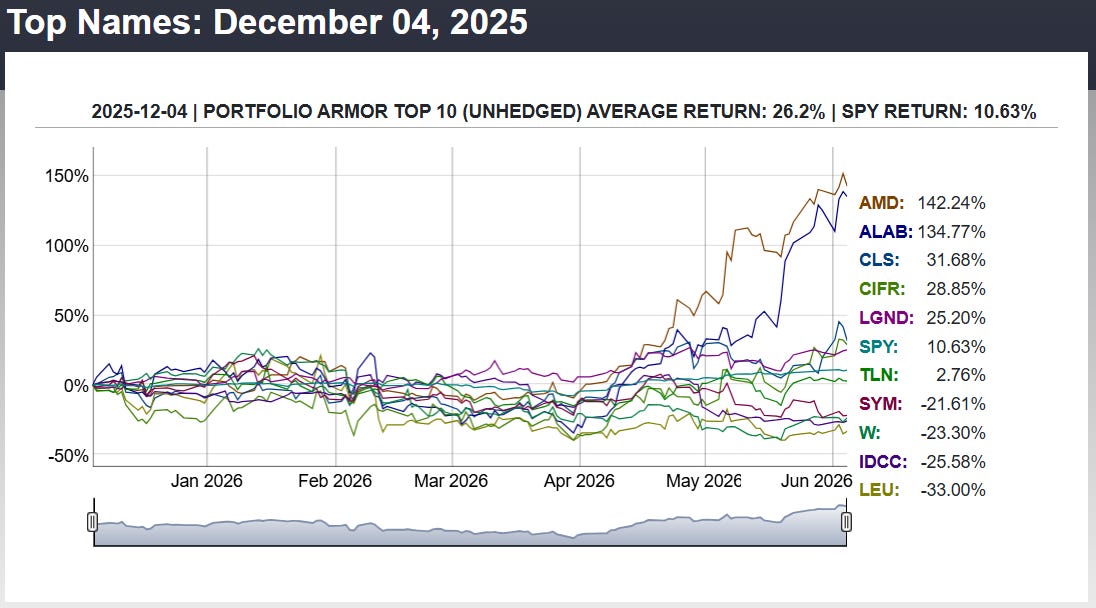

No exits this week, as I haven’t been doing our basic strategy, which involves buying stocks and ETFs, and have been focusing on options instead. Nevertheless, the performance of our system’s top names over the next six months continues to be strong, as you can see below.

Options

Fear, Then And Now

This was another strong week on the options side: 9 exits, 9 winners (our losing options exits tend to collect on OpEx days, because our winners tend to trigger our pre-set exit orders before expiration; you can see examples of those in May's OpEx day Exits post).

That was especially encouraging given today’s market action. When fear dominates the tape, it is easy to focus only on the positions that are moving against you in the moment. But today also gave us a useful reminder of why we put these structures on in the first place.

Two of today’s exits came from our March 25th trade alert, “Fading Fear.”

That was a moment when war-related headlines and market anxiety were elevated, but we were looking for opportunities to add bullish exposure with defined risk, which we did in part by placing trades on Cameco (CCJ 0.00%↑) and iShares MSCI South Korea ETF (EWY 0.00%↑).

Today, in another fear-heavy tape, we closed the remaining EWY calendar for a full 4-leg hybrid combo gain of 177%, and bought back the short call in Cameco for a 96% gain on premium collected. Earlier this week, we also exited the Cameco put spread from that same combo for an 86% gain.

That is the kind of symmetry we want: use fear when it gives us favorable entries, then let the structure do its job.

The Structures Did Their Job

The point of these trades is to start with defined downside, use option premium where it is available, and give the bullish side enough time to work. That mattered today. Despite the shakeout, we were not forced out of any recent options trades, and we did not get assigned on any short puts.

That is not an accident. The recent combos have generally used limited-risk put spreads rather than naked puts, and expirations far enough out that one rough session does not automatically decide the trade.

Sometimes those put spreads or short calls expire worthless. Sometimes we buy them back for $0.20 or less. Either way, when those exits work, they reduce risk and can leave us with cleaner upside exposure.

Premium Harvesting And Big Call-Side Exits

Most of this week’s exits were premium-harvesting exits: put spreads and short calls bought back after most of the value had decayed.

That included put spread exits in NexGen Energy, Cameco, and Twist Bioscience, plus short-call exits in Capricor, Perma-Pipe, and Cameco. Those are not the flashiest exits, but they are important. They lock in income, reduce exposure, and improve the remaining structure.

The bigger headline numbers came from the full combo exits: Sphere Entertainment at 420%, Western Digital at 704%, and EWY at 177%.

Those are three different themes and three different trades, but the same general process: define the downside at entry, resolve the downside hedge when possible, and let the call side do the heavy lifting when the underlying stock or ETF moves our way.

Another Clean Week

This was a clean week: no stock exits, but a full slate of profitable options exits.

Weeks like this show why we keep using these structures. They let us stay aggressive where the upside is attractive, without turning every trade into an all-or-nothing bet.

That is the balance we are trying to strike: disciplined entries, defined risk, and enough upside exposure for the winners to matter.